Ellen MacArthur Foundation policy brief argues current EPR schemes direct materials to recycling when reuse and repair would retain more value, calling for fee structures that incentivise higher-value circular pathways.

Extended Producer Responsibility (EPR) schemes are failing to maximise resource value because they focus on recycling and energy recovery rather than reuse and remanufacturing, according to a policy brief published by the Ellen MacArthur Foundation (EMF).

Although EPR provides dedicated funding to manage products after use, Ellen MacArthur says current schemes channel this towards lower-value pathways. Reuse and repair retain more embedded value than recycling, yet fee structures rarely reflect this hierarchy.

The Foundation calls for eco-modulated fees that vary according to repairability and reusability, not just recyclability. Under such schemes, products designed for longer use and easier repair would attract lower fees than those destined for single use and material recovery.

The UK’s packaging EPR, which came into effect this year is seen as a case in point, While reusable packaging avoids ongoing disposal fees - an inherent advantage - the fee modulation framework does nothing to go further. PackUK's Recyclability Assessment Methodology applies escalating charges for poorly recyclable packaging from 2026, yet offers no additional support for packaging designed for reuse or refill.

Why recycling falls short

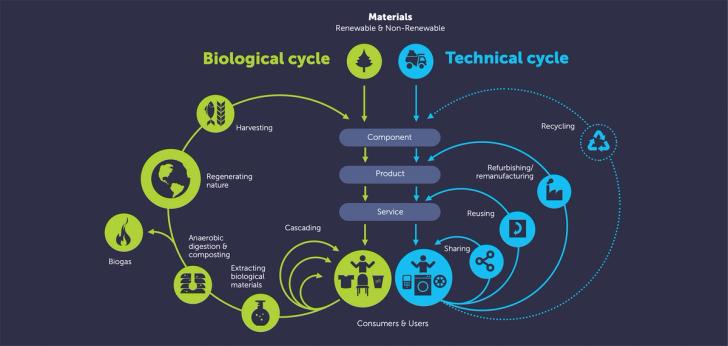

The policy brief sets out the rationale for prioritising reuse over recycling. When products are recycled, they lose the energy and labour embedded during manufacture. A reused product, by contrast, retains this value across multiple use cycles. The Foundation's 'butterfly diagram' framework positions reuse, repair and remanufacturing as inner loops that preserve more value than recycling, which sits further out as a material-level intervention.

This matters economically as well as environmentally. Global resource consumption now exceeds 100 billion tonnes annually, with the UN Environment Programme warning extraction could rise 60 per cent by 2060. Three quarters of extracted materials are non-renewable and recycling alone cannot reverse this trajectory because it still requires energy inputs and generates losses at each cycle.

EMF’s guidance notes that without policy intervention favouring higher-value loops, cost structures and market incentives will continue to favour volume-based sales models over service and reuse models.

Mandatory schemes with robust enforcement

Beyond fee modulation, the Foundation argues that EPR schemes should be mandatory rather than voluntary. Voluntary approaches can inform policy development but tend to be limited in scope, underfunded and fragmented. Mandatory, fee-based schemes provide regulatory clarity and reduce free-riding.

Germany's packaging EPR, operating since 1991, demonstrates what robust enforcement can achieve. The country reached a 96 per cent packaging recovery rate and 69 per cent recycling rate in 2023. The Foundation attributes this to a combination of eco-modulated fees, a public registration database requiring all companies placing packaging on the market to register, and fines for non-compliance reaching up to €200,000.

However, the briefing also notes a limitation: packaging volumes placed on the German market have not declined, indicating that recycling-focused EPR cannot curb overall material use. This reinforces the case for fee structures that incentivise reduction and reuse alongside recyclability.

Waste definitions blocking higher-value pathways

The briefing identifies waste regulations as a second barrier to keeping materials at their highest value. Once a product is classified as waste, strict handling, transport and treatment rules apply. These rules protect human health and the environment but can unintentionally make reuse and repair more complex or costly than disposal.

The Foundation argues that unclear or inconsistent definitions create legal uncertainty that discourages investment in circular business models. A product that qualifies for reuse in one jurisdiction may be classified as waste in another, complicating cross-border trade in secondary materials.

End-of-waste criteria, which specify when a material ceases to be waste and becomes a resource again, can address this problem. The EU Waste Framework Directive established such criteria for iron, steel, aluminium scrap, glass cullet and copper scrap, though uptake across member states remains partial.

According to EMF, Ireland's approach, which allows industry to request end-of-waste decisions for specific materials, offers a model for responsive governance. The country has established criteria for recycled aggregates, road planings and greenfield soil and stone, enabling these materials to re-enter production processes.

The Foundation recommends that governments build institutional capacity to interpret and apply classifications confidently. Without trained staff and clear guidance, enforcement can become overly cautious, leading to materials being prematurely defined as waste.

Secondary materials need demand signals

The third instrument the guidance identifies is policy support for secondary materials markets. Even where materials are collected and processed, they struggle to compete with virgin alternatives on price, quality consistency and supply reliability.

The Foundation argues that pricing interventions can level this playing field. Options include taxes on virgin material extraction or use, subsidies for secondary materials, and public procurement requirements specifying recycled content. Quality standards and certification schemes can address buyer uncertainty about secondary material performance.

Korea's certification system for post-consumer recycled plastics, launched in 2024, demonstrates how standards can build market confidence. The scheme allows companies to certify products meeting minimum recycled plastic thresholds, with labels providing consumers a trusted information source. By recognising international certifications as equivalent, the system reduces compliance costs for exporters.

China's remanufacturing sector shows how national targets can drive scale. The government set a goal of growing the sector to RMB 200 billion (£22 billion) by 2025, supported by pilot programmes across automotive parts, construction machinery and industrial equipment. Automotive remanufacturing sales reached RMB 50 billion (£5.5 billion) in 2021.

Implications for UK policy

The guidance arrives as the UK prepares its first Circular Economy Strategy, expected in autumn 2025. The Circular Economy Taskforce advising on the strategy is chaired by Andrew Morlet, former chief executive of the Ellen MacArthur Foundation.

The Foundation's recommendations suggest that packaging EPR fee modulation should extend beyond recyclability to incorporate reuse criteria. They also point to the need for consistent end-of-waste frameworks that provide legal certainty for secondary materials traders, and pricing mechanisms that address the cost disadvantage faced by recycled content.

The briefing emphasises that these three instruments work as a package. Waste classifications establish legal foundations, EPR creates funding for collection and processing, and market support mechanisms ensure recovered materials find buyers. Without all three, materials may be collected but not reused, or reused but not at scale.

Get our weekly digest

resource.co article ai

How will the government and DMOs address the challenges of including glass in DRS while ensuring a level playing field across the UK?

There's no easy solution to include glass in the DRS while maintaining a level playing field. Potential approaches include a phased introduction of glass, potentially with higher deposits to reflect its logistical challenges. The government and DMOs could incentivise innovation in glass packaging design and subsidise dedicated return points for glass-handling. Exemptions for smaller businesses unable to handle glass might also be necessary. Any successful solution will likely blend several approaches. It must address the differing priorities of devolved administrations, balance environmental benefits with logistical and cost implications, and be supported by robust consumer education campaigns emphasizing the importance of glass recycling.